FAQ

Overview of Topics

Internetbanking

With Internetbanking, you have access to your account any time and you can conduct your financial transactions online, safely and easily at home.

The following functions are available:

The following functions are available:

Electronic bank statements and receipts

Free domestic and EU transfers

Opening Daily Due Deposit and Time Deposit Accounts

High security with mobile TAN

Foreign transfers

Template management for recurring payments

Advanced search for account activities

Account balance queries

Update of contact details

New customers have to register under “Open New Account” on the DenizBank AG website. After

successful registration and verification of your identity, the customers will receive their login information per

post.

If you are already a DenizBank AG customer, please download the Internetbanking Application Form from our website and send us the signed form per post.

If you are already a DenizBank AG customer, please download the Internetbanking Application Form from our website and send us the signed form per post.

Payment- or Daily Due Deposit Account at DenizBank AG

An Email address

Internet access

A mobile phone number

Please use the button "Login Internetbanking" under Private” on the DenizBank AG website to go to

the login page of DenizBank AG Internetbanking. There you need to enter your customer number and your PIN. Joint

account holders have to enter both, the joint account number as well as the private customer number.

New customers receive their log-in data as soon as all their documents are receipted at DenizBank AG. For customers who have registered online, DenizBank AG has to wait for the confirmation of identity verification by the Post AG.

Your PIN will be sent via SMS to the mobile phone number you have registered at DenizBank AG.

When entering your log-in data, please use your own keyboard and make sure you pay attention to upper and lower case letters.

In addition, you must change the PIN you got from DenizBank AG when you first login.

In addition, you must change the PIN you got from DenizBank AG when you first login.

New log-in data can only be ordered in written form. Please use the Internetbanking Application Form under “Customer Service

/ Documents”. Please return the signed application form per post or visit one of our branches

With an "Own Account Transfer" you can transfer your savings between your Payment Account and your Daily Due

Account. This feature can be found in the Internetbanking

under

"Transfers“.

No, "Own Account Transfer" enables you only transactions between your DenizBank AG accounts.

Choose the function “Transfers” in the Internetbanking.

Please note that transfers are only possible from your Payment Account.

DenizBank AG offers this service to its customers free of charge as long as the transaction is made online.

With the “Foreign Transfers“ feature, you can also accomplish transfers outside the EU.

Yes, international transfers are charged with a fee. The current prices for foreign transfers are

listed in our List of Fees.

You can only conduct external transfers from your Payment Account. Please transfer your deposit from your Daily Due Deposit Account to your Payment Account by using the function "Own Account Transfer“. The transfer is completed within a few minutes, so you can conduct further transfers immediately.

Online Saving

Online Deposit Accounts

You can either register on the homepage and apply for a

DenizBank AG account conveniently from home or visit one of our branches.

Once you have registered on the homepage, you will receive an

application form by post. Please send us the signed form with a copy of your identity card per post.

In addition, DenizBank AG has to wait for the confirmation of identity by the Post AG.

The identity confirmation is done via advice of receipt (der IDENT-BRIEF). For this you will receive a printed form of the receipt together with your application documents. You have to sign this form upon receipt of the application documents at the post office. To verify your identity you will need a passport, identity card or driving license. The advice of receipt will then be sent to DenizBank AG per post.

Once we have received these documents, you will get your log-in data via text message sent to the mobile number you have entered in the application form.

If you open a Payment Account at one of our branches , you will receive your log-in data on the same day.

In addition, DenizBank AG has to wait for the confirmation of identity by the Post AG.

The identity confirmation is done via advice of receipt (der IDENT-BRIEF). For this you will receive a printed form of the receipt together with your application documents. You have to sign this form upon receipt of the application documents at the post office. To verify your identity you will need a passport, identity card or driving license. The advice of receipt will then be sent to DenizBank AG per post.

Once we have received these documents, you will get your log-in data via text message sent to the mobile number you have entered in the application form.

If you open a Payment Account at one of our branches , you will receive your log-in data on the same day.

This account enables you to open deposits and offers you additional transfer functions. A Payment Account should not be mistaken with a Daily Due Deposit Account (Savings Account). From your Payment Account, you can open a Daily Due and Time Deposit Accounts. Therefore, the deposit of an external Reference Account is not required.

The prevention of money laundering act (Geldwäschegesetz GWG) obliges us to verify the identity of our customers when opening an account. The advice of receipt (der Ident.Brief) is the most convenient method to verify your identity. You will receive a printed receipt together with your application documents. You will need to sign this form upon receipt of the application documents at the post office.The legitimacy can only be verified with a passport, identity card or driving license. The advice of receipt will then be sent to DenizBank AG by post.

You can withdraw money in all of our branches . Please transfer your money from your Daily Due to your Payment Account beforehand.

Payment Account

This is a base account which enables you to open deposits and offers you additional transfer functions. A Payment Account should not be confused with a Daily Due Deposit Account (Savings Account). From

your Payment Account, you can open a Daily Due and Time Deposit Accounts.

Therefore, the deposit of an external Reference Account is not required.

You can always open a Payment Account in one of our branches. You also have the option to open a Payment Account online.

Please register on our homepage for online saving.

If you are already an online customer at DenizBank AG, you can open a Payment Account in the Internetbanking Portal of DenizBank AG under “Account Management

/ Online Deposits”.

DenizBank offers the Payment Account free of charge. In addition, all online transactions from the Payment Account are also free of charge.

The interest rate is 0.01% p.a. The account statement is issued quarterly.

The Payment Account used as a Reference Account for your deposits and money transfers. In order

start saving, you

have to open a Daily Due or a Time Deposit Account in your Internetbanking Account.

Daily Due Deposit Account

The Daily Due Deposit Account is an Online Deposits Account of DenizBank AG. It offers you

attractive interest rates and instant access to your savings.

The Daily Due Deposit Account is only offered to customers with Internetbanking.

Customers with a Payment Account

can

open a Daily Due Deposit Account using the “Account Management“ and “Online Deposits“ functions in Internetbanking.

You can find the current interest rate of the Daily Due Deposit Account in the list of fees

DenizBank AG offers you the Daily Due Deposit Account free of charge.

DenizBank AG offers you the opportunity to open only one Daily Due Deposit Account.

The minimum deposit is 100 Euro.

You can transfer your deposit directly to your Payment Account. The next step is to open a Daily Due Deposit Account

and transfer the deposit amount onto the Daily Due Deposit Account. You can also deposit your Payment Account at one

of our branches.

Transfers from your Daily Due Deposit Account are not possible. Please use your Payment Account for this purpose. By using “Own Transfer”, you can transfer your deposit from your Daily Due Deposit Account to your Payment Account from where you can conduct further transfers to external accounts.

On December 31st of each year, the accumulated interest will be credited to your Daily Due Deposit Account.

Time Deposit Account

The Time Deposit Account is an Online Deposits Account at DenizBank AG. A specific amount (minimum amount 1.000 Euro) is

invested for a fixed term with fixed interest rates for the whole term. At maturity the interest will be credited to

your account.

In order to open a Time Deposit Account, you need to have a Payment Account at DenizBank AG.

You can open the Time Deposit Account in your Internetbanking account under Online Deposits/Open a Time Deposit Account. Please enter the deposit amount, the debit account (either Payment Account or Daily Due Deposit Account) and the roll over type and confirm your entries with a TAN.

Please log- in the Internetbanking and go to ''Account Management''. Then you choose ''Online Deposits“ and ''Open a Time Deposit Account“. Enter the deposit amount, the debit account (Payment Account or Daily Due Deposit Account of DenizBank AG) and the roll over type. Then confirm your entries with a TAN.

Please note that the deposit must be on your Payment or Daily Due Deposit Account before you open a Time Deposit Account.

You can open the Time Deposit Account in your Internetbanking account under Online Deposits/Open a Time Deposit Account. Please enter the deposit amount, the debit account (either Payment Account or Daily Due Deposit Account) and the roll over type and confirm your entries with a TAN.

Please log- in the Internetbanking and go to ''Account Management''. Then you choose ''Online Deposits“ and ''Open a Time Deposit Account“. Enter the deposit amount, the debit account (Payment Account or Daily Due Deposit Account of DenizBank AG) and the roll over type. Then confirm your entries with a TAN.

Please note that the deposit must be on your Payment or Daily Due Deposit Account before you open a Time Deposit Account.

DenizBank AG offers the following terms:

3 Months

6 Months

9 Months

12 Months

18 Months

24 Months

32 Months

48 Months

60 Months

72 Months

84 Months

96 Months

108 Months

120 Months

The minimum deposit amount is 1.000 Euro.

Please transfer your deposit to your Payment Account and open a Time Deposit Account online.

The accumulated interest will be deposited to your Time Deposit Account at maturity (at the end of the term).

To open a Time Deposit Account, you need to have a Payment Account at DenizBank AG. The deposit you want to invest on your

Time Deposit Account has to be already on your Payment Account.

It should also be noted that you have to choose the roll over type:

It should also be noted that you have to choose the roll over type:

Re-payment at maturity

The amount will be transferred to your Payment Account at maturity.

Re-invest of interests and capital:

The interests and capital will be reinvested for the same term with the interest rate applicable at the time of

maturity.

Re-invest of capital:

The capital will be reinvested for the same term with the interest rate applicable at the time of maturity. The

interests will be transferred to your Payment Account.

You can open an unlimited number of Time Deposit Accounts at DenizBank AG.

According to the roll over option you have chosen, your time deposit is either transferred to your Payment Account or prolonged/re-invested (only principal amount or principal together with the interest amount).

If you do not want to re-invest a written notification is required.

If you do not want to re-invest a written notification is required.

The interest rate of a Time Deposit Account is guaranteed for the whole term.

Time Deposit Account is free of charge.

Please send a written application by post to our Contact Center (Thomas-Klestil-Platz 1, 1030 Vienna) or visit one of our branches.

Payments made prior to the end of the term are to be treated as advances, and interest is to be calculated accordingly. For these advances, 0.1% is to be charged for each full month by which the commitment period is not observed. However, interest on advances must not exceed the total credit interest accrued on the amount accepted; to the extent necessary, charges may be applied retroactively to credit interest paid out in the preceding year in cases where the credit interest for the current year is not sufficient. Any reduction of a commitment duration will also trigger interest on advances. Furthermore, point IV.6. of the Special Terms and Conditions for Online Saving applies.

Deposit Insurance

DenizBank AG is a member of the Austrian deposit insurance. The deposits of natural and non-natural individuals are secured

up to a maximum of 100,000 Euro(per depositor and bank). For certain special conditions, such as "temporary limited

covered deposits" (E.g. Deposits from Real Estate transactions of privately used Residential Real Estate; payments of

insurance benefits or compensation for criminal offenses; payments which fulfill the statutory purposes - more detailed

information can be found on the homepage of the Deposit Insurance, www.einlagensicherung.at) can be made within 12

months after the insurance claim application at the Protection Scheme executed that the deposit is to be reimbursed up

to an amount of 500,000.00 Euro.

The deposit guarantee always applies per depositor (individuals /non-natural persons), regardless of how many accounts or savings books the depositor has at the institution in question.

For individuals, the deposit guarantee for deposits at any bank is up to 100,000 Euro per depositor per bank.

With the deposit insurance, there is no deductible (either for individuals or for non-natural persons). When it comes to

investor compensation, a deductable in the amount of 10% of the claim is valid for non-natural persons. Further

information on the topic of investor compensation is available at the legal regulations (§§ 44 ff ESAEG) and the

homepage “https://www.einlagensicherung.at”.

All balances on accounts or savings books, such as salary and pension accounts, other current accounts, fixed deposits, capital or overnight savings accounts are covered by the deposit guarantee. Credit balances in foreign currencies will be made in Euro in the event of occurrence of deposit guarantee case (Conversion rate is the exchange rate on the date of the hedge).

Deposits of underage persons are also subject to the statutory deposit insurance.

By trust accounts, where the assets are held by individuals other than the invester, the payment is made after the legitimacy and proof of the claim to ensure that the maximum amount is used for the benefit of the beneficial owner. Among the occupational groups which may open the trust account fall: lawyers, notaries, trustees, property managers and brokers, architects and engineering consultants.

No, a withdrawal from the relevant protection scheme is only permitted if the institution concerned joins a different protection scheme, which means it changes the sector. The statutory guarantee must be ensured without interruption in any case, as no guarantee would lead the bank to lose its license.

Since 01.01.2019 there are two protection schemes in Austria:

„Einlagensicherung AUSTRIA Ges.m.b.H.“ (ESA) as a uniform, cross-sectoral security scheme established at the Austrian Federal Economic Chamber

"Sparkassen-Haftungs GmbH" as an institution-related security system, which is officially recognized as a security institution

Following examples of deposits or claims are not secured (for details see § 10 Abs. 1 ESAEG):

Bonds of a credit institution and liabilities from own acceptances. Deposits of pension and retirement funds as well as of insurance companies and reinsurance undertakings.

Deposits for which the identity of the holder has never been established until the date of the occurrence of a deposit guarantee case, unless the holder takes such action within 12 months after the occurrence of a deposit guarantee case.

Deposits and receivables of states as well as deposits and receivables of regional and local authorities (eg, state and local)

All claims by the investor against the credit institution, in particular:

No claim to double compensation. Claims both covered deposits and safety obligated claims from securities will be compensated by the Deposit Guarantee Scheme (Section 51 (1) ESAEG).

Administration and custody of securities (custody business)

Trade of the credit institution with financial market instruments

Returns from securities settlement (dividends, sales proceeds, redemption, etc.) are protected as deposits on a customer account within the framework of the insurance of claim up to a maximum amount of 100,000.00 Euro.

No claim to double compensation. Claims both covered deposits and safety obligated claims from securities will be compensated by the Deposit Guarantee Scheme (Section 51 (1) ESAEG).

As the owner of the securities kept in the securities account (stocks, bonds, mutual funds, etc.), the customer can -in the case of a bancruptcy of the custodian bank - make a claim rejection on these securities claims (in full), ie securities owned by him do not fall into the bankruptcy of the custodian bank. Securities which are kept in the securities account are not secured themselves (there is the risk of bankruptcy of the issuer).

The security ceiling

On deposit insurance see item 1), investor compensation is unmodified and is 20.000 Euro per investor (natural or non-natural person) per bank

On deposit insurance see item 1), investor compensation is unmodified and is 20.000 Euro per investor (natural or non-natural person) per bank

The retention

Only by investor compensation in non-natural persons, unchanged at 10% of the claim

Only by investor compensation in non-natural persons, unchanged at 10% of the claim

Different Payment Deadlines

In case of Investor Compensation within 3 months, in case of Deposit Guarantee within 7 working days.

In case of Investor Compensation within 3 months, in case of Deposit Guarantee within 7 working days.

In the event of the claim of insurance, it is allowed to refund the covered deposit at the

occurrence of a deposit guarantee case without the need of an application by the investor (exception: investor

compensation and temporarily limited covered deposits due to the law § 12 Austrian Banking Act).

Each protection scheme (a single protection scheme and institution-related protection systems) has a deposit guarantee fund in the amount of 0,8% of the total amount of covered deposits, and as long as the Member Institutions require annual contributions and other contributions to prescribe to the target amount is reached.

If the affected protection scheme detected, the reimbursement of covered deposits from the fund assets which is not included in the statutory payment periods (see point 13) can be secured, so the other protection schemes are immediately informed and pay these for the cover of the shortfall (§§ 18 ff ESAEG).

If the affected protection scheme detected, the reimbursement of covered deposits from the fund assets which is not included in the statutory payment periods (see point 13) can be secured, so the other protection schemes are immediately informed and pay these for the cover of the shortfall (§§ 18 ff ESAEG).

In the event of bankruptcy of a financial institution, the customer can compensate for its claims against the bank (eg deposit) with its liabilities to the bank (eg from loans). E.g. a loan of 50,000 Euro is offset by a deposit in the amount of 50,000 Euro. Thus, the customer suffers no harm in such a case, as claim and liability are balanced by compensation. If the customer in the example above had no claim against the deposit insurance, a shortfall would be present.

The credit institutions which are committed to in accordance with § 38 ESAEG should inform their customers through the announcement in the cashier´s hall and from their home page about the regulations of deposits insurance in which protection scheme is affiliated with. Customers are informed about the deposit protection by means of the information sheet (in accordance with section 37a BWG). This information sheet is provided to the depositor at least once a year.

The deposit guarantee applies per customer (depositor), not per account. In a jointly controlled account each account holder has a basic claim for compensation.

In principle, the assignment of the balances of the joint account is based on 1:1 allocation. However, it is free to the account holders to hand over a written regulation to the credit institute before the admission of insurance claim which deviates from the 1: 1 allocation. In the event of occurrence of a deposit, then the selected allocation key should be used for this assignment.

Deposits in accounts of open societies (OG), limited partnerships (KG) or civil partnerships (GesbR) and foreign companies corresponding to these kinds of companies are always treated as deposits of a person, even if there is more than one shareholder. In this case, the maximum payment amount is therefore 100,000 Euro in total.

In principle, the assignment of the balances of the joint account is based on 1:1 allocation. However, it is free to the account holders to hand over a written regulation to the credit institute before the admission of insurance claim which deviates from the 1: 1 allocation. In the event of occurrence of a deposit, then the selected allocation key should be used for this assignment.

Deposits in accounts of open societies (OG), limited partnerships (KG) or civil partnerships (GesbR) and foreign companies corresponding to these kinds of companies are always treated as deposits of a person, even if there is more than one shareholder. In this case, the maximum payment amount is therefore 100,000 Euro in total.

Securities from the Custodian bank will only be kept and always remain in the property of the customer. With the request, the securities will be followed or transferred to another depot.

smsTAN Verification

A TAN (transaction number) is a one-time password (OTP) used in Internetbanking to verify transactions.

The smsTAN Verification is a two-way authorization procedure. When you want to place an order you receive your TAN only if required via SMS directly to your mobile phone. . This TAN is valid only for a few minutes and just for this transfer. The transaction will be completed after entering the TAN into the specified field.

The delivery of the SMS is free of charge. Please note that when a smsTAN is delivered abroad, a roaming fee may be charged by your provider.

You can choose one of 3 options to change your phone number:

a. By post

Just send an informal signed letter with your new phone number to DenizBank AG, Thomas-Klestil-Platz 1, 1030 Wien.

Just send an informal signed letter with your new phone number to DenizBank AG, Thomas-Klestil-Platz 1, 1030 Wien.

b. Per Fax

If you have indicated during the account opening that you also want to give orders by fax, you can change your number in this way.

If you have indicated during the account opening that you also want to give orders by fax, you can change your number in this way.

c. In a branch

You can also visit us in one of our 11 branches all over Austria. Our staff will be happy to assist you.

You can also visit us in one of our 11 branches all over Austria. Our staff will be happy to assist you.

pushTAN Verification

Since the strong customer authentication came into force, the login to your DenizBank AG internetbanking has been protected not only by entering your PIN, but also by an smsTAN or pushTAN. The smsTAN or pushTAN will be sent to you when you log in to the mobile number you have provided or to the mobile device connected to your account.

S€PA – Payment transactions without borders

SEPA (Single Euro Payments Area) is standardizing cashless payment transactions within Europe.

The participating countries include the 28 EU Member States plus Norway and Liechtenstein as Member States of the European Economic Area (EEA), together with Monaco and Switzerland.

As of 1 February 2014, SEPA will likewise change the cashless payment transaction system in Austria. Banks and savings institutions (Sparkasse) are required to execute transfers and direct debits made in Euro in accordance with a standardized European-wide scheme.

The IBAN (International Bank Account Number) replaces your account number; the BIC (Business Identifier Code) replaces your bank code.

Would you like more information about SEPA or do you have any particular questions?

For more information, please read

The participating countries include the 28 EU Member States plus Norway and Liechtenstein as Member States of the European Economic Area (EEA), together with Monaco and Switzerland.

As of 1 February 2014, SEPA will likewise change the cashless payment transaction system in Austria. Banks and savings institutions (Sparkasse) are required to execute transfers and direct debits made in Euro in accordance with a standardized European-wide scheme.

The IBAN (International Bank Account Number) replaces your account number; the BIC (Business Identifier Code) replaces your bank code.

Would you like more information about SEPA or do you have any particular questions?

For more information, please read

FAQ Private Customers

The conversion to the single payment area affects everyone who has an account with a Bank – irrespective of whether they are an individual person, an association, an enterprise or a public institution.

The SEPA conversion will not cost private customers anything.

Yes, SEPA means more security for payment transactions. Take direct debit collection mandates for example - the payee can be unambiguously identified through the new creditor identifier. Assigned in Austria by the Oesterreichische Nationalbank, the consumer can see the creditor identifier both in the SEPA direct debit collection mandate and in the account statement – or online in the account payments history display, all of which creates greater transparency.

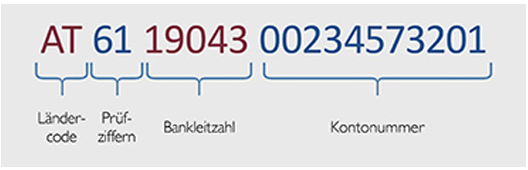

TheIBAN is easy to notice, because it is made up of the 11-digit account number and the 5-digit bank (sort) code, together with the national code AT for Austria and a 2-digit verification number. That means that, other than these four characters, the IBAN is uniquely assigned to you.

Quelle: Österreichische Nationalbank

Your new, 20-digit account number is now displayed on your account statements (top right-hand

corner). When banking online, you can get your IBAN at »Account Management« › »Account Information« › »Account

Detail«. Or use our free smartphone app with its practical IBAN computer - simply enter your account number and

you're good to go!

The international exchange of data between banks is regulated by the "Society for Worldwide Interbank Financial

Telecommunications" (SWIFT). It assigns every participating bank a unique international bank ID, known as the "Bank

Identifier Code" (BIC). The BIC consists of eight or eleven characters. It is made up of

The BIC for DenizBank AG is: ESBK AT WW

the 4-digit bank code

the 2-digit country code

the 2-digit location code

the 3-digit code for the branch or department (optional).

The BIC for DenizBank AG is: ESBK AT WW

No, we will convert your standing orders to be ready for SEPA.

Starting from 1 February 2014, you will begin using the IBAN instead of your previous account number and bank code. The IBAN is sufficient when making payments inland (BIC not needed). The BIC will still be needed when making international payments (foreseeably until February 2016).

Cross-border transfer charges are more cost-effective with SEPA - a SEPA transfers costs the same as an inland bank transfer, dependent of course on the specific terms of the particular account.

No, they are the same. Within the Eurozone, the transferred sums have to arrive in the target account within one banking day.

There is a new pre-printed form for Euro transfers, which you can obtain in our branch offices. You can also make payments easily using your online banking access.

Within Austria, goods and services are frequently paid for using a direct debit collection mandate (Einzugsermächtigung). As a consumer, you will certainly be familiar with these when making payments to your energy supplier. For the first time, the new SEPA Direct Debit Scheme enables due invoiced sums to be collected by direct debit not only with Austria, but also across borders within SEPA. Payees that use the SEPA direct debit method will need you to provide them with a SEPA direct debit collection mandate. However, as the payer there is no need for you to act. It is the responsibility of the payee to approach you to obtain the direct debit collection mandate.

Only direct debits issued in writing will remain valid after 1 February 2014. In future, your account statements will provide you with additional information such as the creditor identifier and a mandate reference (e.g. an invoice number or a membership number of the association). New direct debits will use SEPA mandates, standardised in all SEPA countries.

No. Direct debit mandates only have to be re-issued if the payee explicitly requests this from the customer.

As with the previous direct debit collection mandate, you are able here to arrange payments to be made to a payee. If you are the payee, agree a suitable mandate for this purpose and collect the payment using the SEPA Core Direct Debit. You can use the SEPA Core Direct Debit if your payment partner's bank also supports this scheme. DenizBank AG is part of the SEPA Core Direct Debit Scheme.

If an amount is ever debited from your account and you do not agree to it, you can object to it within a period of 8 weeks from the date of the debit entry (due date). You have the right to demand reimbursement of the direct debit amount without being required to state any reasons.

We will attend to the conversion of your standing orders and bank transfer slips on your behalf.

No, DenizBank AG will automatically attend to the IBAN and BIC conversion of the reference account (e.g. for direct debit payment collections or savings deposits).

No, there will be no change to your online banking log-in data (account number and PIN). Please continue to use your current details!

FAQ Corporate Customers

If you are paying an invoice, then you can read the IBAN and BIC from your business partner's invoice or letterhead. If you are unable to find the information you need from there, please contact your business partner directly.

As a payee or direct debit creditor, you will need a creditor identifier (or CI) to use the Euro direct debit based on the SEPA Direct Debit Scheme. This code is valid throughout all of SEPA, and it uniquely identifies you as a direct debit creditor.

In Austria you can apply to the Oesterreichische Nationalbank (OeNB) for your creditor identifier. If you have any questions, please contact your customer adviser – they will be glad to assist you further.

There is a new pre-printed form for Euro transfers, which you can obtain in our branch offices. You can also make payments easily using your online banking access.

There will no longer be pre-printed forms for national direct debit schemes, because submissions will usually be made electronically. As direct debit creditor, you can make your direct debit payment collections simply via your online banking account. Our advisors are ready and will to help you. Simply ask.

As of right now, you can use the new SEPA Direct Debit Scheme to collect payments - both inland and across borders using the SEPA Core Direct Debit, or if you are a corporate customer you can also use the SEPA B2B Direct Debit Scheme. The new SEPA Direct Debit Scheme is similar to that of the Austrian Einzugsermächtigung (direct debit collection mandate) and the Abbuchungsauftrag (a type of direct debit authorisation). It is based on direct debit collection mandates issued by the relevant payers.

The direct debit collection mandate can in future also be used for the SEPA Core Direct Debit. This negates any need for payees to go to the effort of obtaining SEPA direct debit collection mandates for existing debit collection authorisations. Another advantage is that under SEPA, direct debit payments under the direct debit authorisation scheme are now also insolvency-proof.

As is already the case with the SEPA Direct Debit Scheme, Section 45 Payment Services Act applies to the direct debit collection mandate procedure following the change. A standard reimbursement period of 8 weeks applies from the date of the debit entry – without any need for stating reasons. This also makes direct debit payments under the direct debit authorisation scheme insolvency proof.

No, direct debit creditors will be able to collect direct debit payments under the direct debit authorisation scheme as before.

For the payee the direct debit collection mandate is the instruction to collect amounts from the specified bank account via direct debit payment collections. For the bank of the payee, the direct debit collection mandate constitutes an instruction to redeem the direct debits of the payer. With the SEPA Core Direct Debit Scheme the direct debit collection mandate is known as the "SEPA direct debit collection mandate", in the SEPA B2B Direct Debit Scheme it is known as the "SEPA B2B direct debit collection mandate".

To ensure that direct debit payment collections are successfully executed, direct debit creditors are obliged to notify the payee of the amount and date of the payment before it is actually collected. This enables the payee to ensure that an appropriate sum is available on its account. If both parties have not made any other agreement, the payee must inform the payer of the pending direct debit 14 days ahead of its due date. A comparable procedure is already customary today. Alternative agreements can also be made between the payer and creditor regarding the pre-notification. For example, it may be sufficient to give notice of the direct debit by way of a comment on an invoice (as is the case today).

As a rule, the pre-notification must be dispatched at least 14 days prior to the due date. However there is the option for the payer and the payee to agree a shorter time period.

A SEPA Core Direct Debit will be authorised once the corresponding direct debit collection mandate has been signed. A SEPA Core Direct Debit is therefore deemed to be authorised in a legal sense even without pre-notification. As an obligation within a payments collection agreement, the dispatch of a pre-notification must be observed regardless. The payee should note the possible consequences of failure to issue a pre-notification, such as repayment due to lack of sufficient funds in the account or by way of a demand for the reimbursement of authorised payments. It is in the interests of the direct debit creditor that the payer be informed in good time prior to the due date or debit date of the direct debit payment collection, to enable it to ensure that sufficient account funds are available. This procedure likewise corresponds to current practice.

We will attend to the conversion of your standing orders and bank transfer slips on your behalf.

No, DenizBank AG will automatically attend to the IBAN and BIC conversion of the reference account (e.g. for direct debit payment collections or savings deposits).

No, there will be no change to your online banking log-in data (account number and PIN). Please continue to use your current details!

Everything you need to know about the IBAN!

Use our Smartphone-App and its practical IBAN calculator. Simply enter the account number and you're good to go! For more information or an

appointment please get in contact with us. Call our Contact Center 0800 88 66 00. We will be happy to assist you!

Bildquelle: European Payments Council

Bildquelle: European Payments Council

If you have further questions, please call our toll-free number 0800 88 66 00 or submit us your question by filling out the

Contact Form.